For decades, American workers have paid into the Social Security system with the quiet confidence that their retirement, disability, or survivor benefits would be there when needed. That confidence, however, is beginning to erode. The phrase social security insolvency is no longer a fringe warning from doomsayers; it is a projected financial reality printed in the annual reports of the Social Security Board of Trustees. Understanding what social security insolvency actually means is crucial, because the term itself is often misunderstood. It does not mean the system vanishes overnight. It does not mean benefits go to zero. But it does signal a fundamental shift in how the program will operate, likely within the next decade.

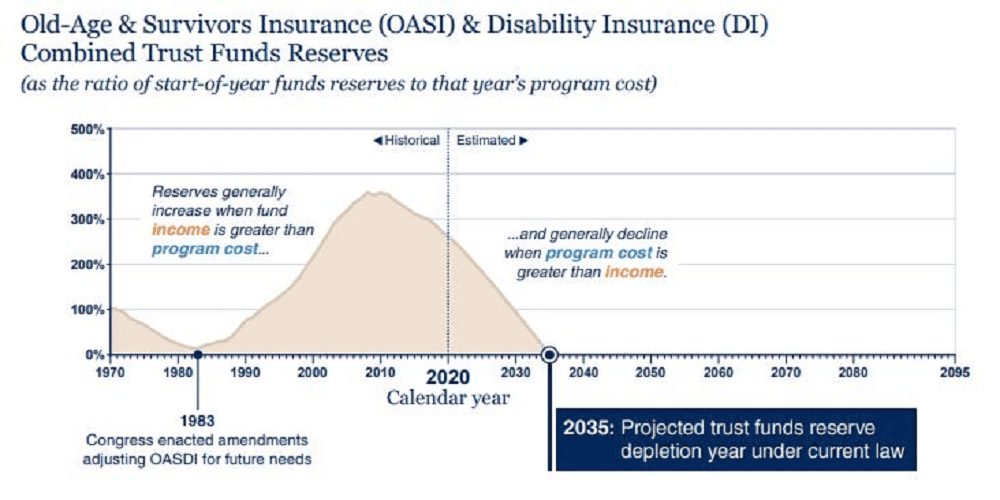

The mechanics of the crisis are not complicated, though the solutions are politically fraught. Social security is largely a pay-as-you-go system. Current workers pay payroll taxes, and that money goes directly to current beneficiaries. For years, the system collected more than it paid out, creating a trust fund surplus. That surplus was invested in special-issue government bonds. Now, the demographic reality has flipped. Baby boomers are retiring in record numbers. Birth rates are below replacement levels. Life expectancy has increased. Consequently, the ratio of workers to beneficiaries has collapsed from over 16 to 1 in 1950 to roughly 2.7 to 1 today. The result is that the trust funds are being drawn down. According to the 2024 Trustees Report, the combined trust funds will be able to pay full benefits only until 2035. After that, social security insolvency—defined as the depletion of those reserve funds—will force an automatic reduction in payable benefits to about 83% of scheduled amounts.

This is the heart of the matter. Social security insolvency does not mean bankruptcy. The federal government cannot go bankrupt in the traditional sense because it controls its own currency. But it does mean a legal constraint will kick in. Under current law, once the trust funds are empty, the Social Security Administration can only pay out what it collects in real-time payroll taxes. That revenue is sufficient to cover roughly four-fifths of current promised benefits. So a young worker planning for retirement in 2040 needs to understand that without legislative changes, their expected monthly check could be cut by nearly one-fifth overnight. That is the practical face of social security insolvency.

Why has this problem been allowed to fester? The answer is a combination of political gridlock and the painful nature of the remedies. There are really only two levers to pull. One is to increase revenue. The other is to reduce spending. In the context of social security, that means raising taxes, raising the retirement age, cutting benefits, or some blend of all three. No politician wants to be the one to tell seniors their benefits are being reduced, nor do they want to tell younger workers their taxes are going up. So the issue has been kicked down the road for three decades. The irony is that waiting has made the necessary adjustments more severe. If lawmakers had acted in the 1990s, small tweaks would have sufficed. Now, because social security insolvency is nearly upon us, the required changes are larger and more disruptive.

It is important to separate fear from reality. Many alarmist headlines suggest the entire system will collapse. That is false. The Social Security Administration is remarkably efficient at sending out checks; it will continue to do so. But the amount on those checks will change. For retirees who depend on social security for more than 90% of their income—and roughly one in five seniors does—a 17% to 20% cut would be catastrophic. Those seniors would face impossible choices between food, medicine, and housing. For higher-income retirees, the cut might mean fewer vacations or less discretionary spending. The point is that social security insolvency hurts the poor the most, as is always the case with across-the-board benefit cuts.

What about younger generations? A millennial or Gen Z worker might look at this and think, “Why should I care? I’ll never see a dime.” That cynicism, while understandable, is not entirely accurate. Even under a insolvency scenario with an automatic benefit cut, future retirees would still receive benefits. They would just receive less than currently promised. Furthermore, the mere threat of social security insolvency has economic ripple effects today. It depresses consumer confidence. It makes long-term financial planning a guessing game. It also fuels political movements that propose radical alternatives, such as privatization or a complete overhaul of the payroll tax system.

Several common misconceptions need to be cleared up. One is that the social security trust fund is full of “worthless IOUs.” This is a talking point from both the far left and far right, but it is misleading. The trust fund holds special-issue Treasury bonds, which are backed by the full faith and credit of the U.S. government. The government has always paid its debt. However, the catch is that redeeming those bonds requires the Treasury to raise funds through taxes, borrowing from the public, or cutting other spending. So the real question is not whether the bonds are valid, but whether the political system will honor them by transferring general revenue into the Social Security system. That is a political decision, not a financial one. Social security insolvency as defined by trust fund depletion is essentially the point at which the government must make that political decision explicitly.

Another misconception is that immigrants are draining the system. The data suggests the opposite. Most immigrants are younger and of working age. They pay payroll taxes for many years before claiming benefits, if they claim benefits at all. Undocumented workers often pay payroll taxes through fake or stolen Social Security numbers but cannot legally claim benefits. This actually subsidizes the system. In fact, a more open immigration policy is one of the few demographic levers that could slow the progress toward social security insolvency. More workers mean more tax revenue without immediate benefit claims.

So what are the actual proposed solutions? They fall into several categories. The first and simplest is to raise the payroll tax cap. Currently, wages above $168,600 are not subject to the Social Security payroll tax. Eliminating that cap entirely or raising it substantially would pour hundreds of billions of new revenue into the system overnight. The political objection is that this would be a massive tax increase on high earners and small business owners. The counterargument is that it would also make the system more progressive, as high earners receive a much lower replacement rate from Social Security relative to their lifetime contributions.

The second solution is to raise the full retirement age. When Social Security was created, the retirement age was 65, and life expectancy was roughly 63. Now, life expectancy is 77, but the retirement age has only crept up to 67. Raising it to 68, 69, or even 70 would reduce the number of years a typical retiree draws benefits. The political problem here is that this is a benefit cut for everyone, and it hurts blue-collar workers with physically demanding jobs the most. They often cannot work into their late 60s.

The third solution is to change the benefit formula. Options include reducing cost-of-living adjustments by using a different inflation index, or means-testing benefits so that wealthy retirees receive less or nothing. The political challenge with means-testing is that it would transform Social Security from a universal social insurance program into a welfare program, potentially reducing political support for it over time.

The fourth and most politically toxic solution is to increase the payroll tax rate across the board. Currently, employees and employers each pay 6.2%. Raising that to 7.2% or 8.2% would cover the shortfall, but it would also reduce take-home pay for every working American and increase labor costs for employers. In a tight economy, that could suppress hiring.

None of these solutions are popular. That is why social security insolvency continues to approach like a slow-motion train wreck. The most likely outcome is a last-minute legislative compromise that blends several of these options. For example, Congress could raise the cap slightly, raise the retirement age by two years over two decades, and trim cost-of-living adjustments. That package would likely be enough to restore solvency for another 30 or 40 years, at which point the next generation would face the same debate.

But what should an individual do in the face of this uncertainty? Financial advisors increasingly recommend a “plan for the worst, hope for the best” approach. For workers under 40, that means not relying on Social Security as a primary retirement income source. Treat any future benefit as a bonus rather than a foundation. Max out 401(k) contributions, fund IRAs, and consider building a taxable brokerage account. For workers over 50 who are closer to retirement, the calculus is different. They are more likely to be protected because any benefit cuts are phased in gradually, typically affecting younger beneficiaries first. A 55-year-old today will likely receive close to full promised benefits. A 35-year-old should assume a 20% to 25% reduction.

There is also the question of disability benefits. The Social Security Disability Insurance trust fund faces a separate but related timeline. It is projected to be depleted earlier than the retirement fund. If that happens, disability benefits would also be cut automatically. This is an overlooked aspect of social security insolvency that affects millions of Americans who cannot work due to severe medical conditions.

The psychological dimension is just as important as the financial one. The term “insolvency” triggers fear and anger. People feel that they have paid into the system their entire working lives and that the government has stolen from them. That anger is understandable but misdirected. The money they paid was never sitting in a personal account. It was used to pay their parents’ and grandparents’ benefits. The promise is that when they retire, their children and grandchildren will pay for them. The problem is that there are fewer children and grandchildren per retiree. This is not fraud or mismanagement. It is simple demographics. But demographics feel like betrayal when you are the one facing a reduced check.

Looking globally, the United States is not alone. Nearly every developed country faces a similar pension crisis. Germany, Japan, Italy, and France all have aging populations and strained pay-as-you-go systems. Some have already raised retirement ages substantially. Others have introduced mandatory private savings accounts. The U.S. has the advantage of a stronger demographic profile than Japan or Italy, but it has the disadvantage of a highly polarized political system that struggles to pass long-term fixes. The window for a gradual, painless fix is closing rapidly. By 2035, the conversation will no longer be about preventing social security insolvency but about managing its consequences.

One under-discussed aspect is the effect on state and local governments. Many public pension systems assume that their retirees will also receive Social Security. If Social Security benefits are cut, those retirees will demand higher payouts from their state pensions, potentially bankrupting cities and counties that are already underfunded. Similarly, disabled veterans who also receive Social Security Disability would see their total income drop. The ripple effects extend far beyond the direct beneficiaries.

So what can an ordinary citizen do about social security insolvency beyond personal financial planning? The answer is to become an informed voter. Understand which candidates support which specific fixes. Vague promises to “save Social Security” mean nothing. Ask specific questions: Do you support raising the payroll tax cap? Do you support raising the retirement age to 70? Do you support means-testing? The answers will tell you whether a candidate has a serious plan or just empty rhetoric. Additionally, participate in the public comment process when the Social Security Administration releases its annual reports. Write to your members of Congress. They need to hear that inaction is not acceptable.

In summary, social security insolvency is a serious but manageable problem. It does not mean the end of the program. It does mean that without legislative action by 2035, benefits will be cut by roughly 17%. The solutions are known and mathematically straightforward, but they require political courage. For individuals, the wise course is to diversify retirement income sources, stay informed, and avoid panic. The system will not collapse. But it will change, and the time to prepare for that change is now, not in 2035 when the trust fund runs dry.

FAQs on Social Security Insolvency

Q: What year will social security insolvency actually happen?

A: According to the 2024 Social Security Trustees Report, the combined Old-Age and Survivors Insurance and Disability Insurance trust funds are projected to be depleted in 2035. At that point, without legislative changes, the system will only be able to pay about 83% of scheduled benefits from ongoing payroll tax revenue.

Q: Will I get zero benefits if social security insolvency occurs?

A: No. This is the most common misconception. Insolvency means the trust fund reserves are empty, not that the system stops functioning. Payroll taxes continue to flow in, so benefits continue to be paid. They are just reduced to the level that current tax revenue can support, which is approximately 83% of promised benefits.

Q: Does social security insolvency affect current retirees?

A: It could, but usually benefit cuts are phased in gradually to protect those closest to retirement. However, if Congress does nothing until 2035, the automatic cut would apply across the board to all beneficiaries, including current retirees. That is why most experts expect a legislative fix before 2035 that grandfathers in older recipients.

Q: Can the government just borrow its way out of social security insolvency?

A: In theory, yes. The government could authorize the Treasury to inject general revenue into the Social Security trust funds. That would effectively mean funding benefits through deficit spending. The political resistance is that this would add trillions to the national debt and would face strong opposition from fiscal conservatives.

Q: How does the payroll tax cap affect social security insolvency?

A: Currently, wages above $168,600 are not taxed for Social Security. Approximately 94% of workers earn below this cap. Raising or eliminating the cap is the single largest revenue-raising option available. If the cap were removed entirely, the shortfall would be eliminated for decades. Opponents argue it would disincentivize high earners and small business owners.

Q: Will the retirement age increase to address social security insolvency?

A: It is one of the most frequently proposed solutions. The full retirement age is already rising to 67 for those born after 1960. Proposals include raising it to 68, 69, or even 70. Each one-year increase reduces long-term shortfall by roughly 5%. The trade-off is that it acts as a benefit cut for everyone, especially those in physically demanding jobs.

Q: Are younger workers going to be hit hardest by social security insolvency?

A: Yes, under most reform scenarios. When changes are made, they are typically structured to protect current and near retirees. For example, a retirement age increase would apply only to those under 50 or 55. That means millennials and Gen Z will likely see the most reduced benefits or the latest retirement ages.

Q: What happens to disability benefits under social security insolvency?

A: The Disability Insurance trust fund has its own depletion date, currently projected slightly earlier than the retirement fund. If both funds are combined in the depletion analysis, the 2035 date applies. Disability beneficiaries would face the same 17% cut unless specific legislative protection is provided.

Q: Can I opt out of Social Security to avoid the insolvency problem?

A: Not as a regular employee. Social Security is mandatory for almost all workers in the United States. Certain state and local government employees may be in alternative pension systems, and some religious groups have exemptions. For the vast majority of private sector and self-employed workers, opting out is not legally permitted.

Q: What is the most likely outcome for social security insolvency?

A: Based on historical precedent, Congress will wait until the last possible moment—probably 2033 or 2034—and then pass a bipartisan compromise. That compromise will likely include a modest increase in the payroll tax cap, a very gradual increase in the retirement age to 68 or 69, and a slight modification to the cost-of-living formula. The cuts will be phased in over 20 years. It will not be elegant, but it will be enough to push the insolvency date another 30 years into the future.

Leave A Comment

0 Comment